Beginning

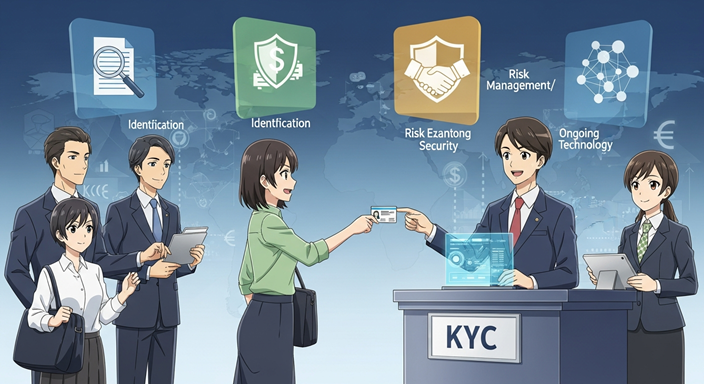

Know Your Customer (KYC) is a very important process for businesses, especially those in the financial sector, to make sure they are who they say they are. It is the foundation of following the rules and helps businesses stop illegal activities like money laundering, fraud, and funding terrorism. As financial crime around the world gets more complicated, KYC procedures have become more and more important for making sure that people can trust and feel safe in the financial system.

What does KYC mean?

KYC stands for the rules and best practices that businesses use to find out who their customers are and make sure they are who they say they are. The process usually includes gathering and checking documents like government-issued IDs, proof of address, and sometimes even biometric data. KYC is not something that happens once; it is an ongoing process that may include regular updates and reviews of customer information.

Important Parts of KYC

Customer Identification Program (CIP)

This is the first step, where businesses gather basic information about the customer, such as their name, address, date of birth, and identification number, to make sure they are who they say they are.

Customer Due Diligence (CDD)

CDD means figuring out how risky a customer is based on their background, financial activities, and transaction patterns. High-risk customers may need more due diligence (Enhanced Due Diligence – EDD).

Ongoing Monitoring

Banks and other financial institutions keep an eye on transactions all the time to look for any suspicious activity that could be a sign of fraud or money laundering.

What is the point of KYC?

Regulatory Compliance

Governments all over the world have passed laws that require banks and other financial institutions to have KYC programs. Not following the rules can lead to harsh punishments, legal problems, and damage to your reputation.

Risk Management

KYC helps businesses figure out and deal with the risks that come with working with customers. Institutions can spot possible illegal activities early and take steps to stop them by getting to know their customers.

Building Trust

Proper KYC procedures help build trust between businesses and their customers, making sure that real customers can easily and safely use financial services.

Problems with KYC Implementation

KYC has some problems, even though it has some benefits:

Costs of Operation

For smaller institutions, setting up thorough KYC processes can take a lot of time and money.

Customer Experience

Long or complicated verification processes may turn away potential customers or make current ones angry.

Changing Threats

KYC procedures must always change to keep up with new risks and technologies as financial crimes change.

The Future of KYC

The future of KYC is being shaped by new technologies. Blockchain, Artificial Intelligence (AI), and automation are making processes easier, cheaper, and more accurate. Digital KYC solutions make it easier for customers to confirm their identities from a distance, which makes things safer and more convenient.

In Conclusion

KYC is still a key part of the modern financial system because it makes sure that everyone follows the rules, lowers risk, and builds trust. As rules and technology change, businesses that want to do business safely and efficiently around the world will need to make sure they are following the best KYC practices.