Why Stablecoins Are Important: An Introduction

Stablecoins are digital tokens that are meant to keep their value stable compared to a fiat currency. They have become a point of conflict between traditional finance and cryptocurrency innovators.

These coins are slowly becoming more common in everyday transactions and a wider range of financial services. This is forcing old-fashioned banks to rethink how money works in the digital age.

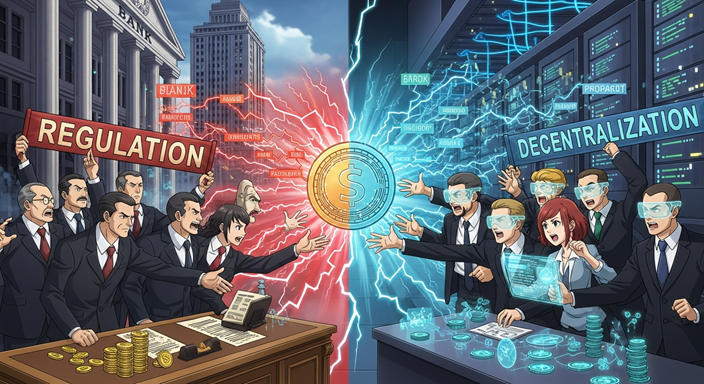

The fight isn’t just about technology; it’s also about who makes the rules and how quickly the system can change without losing security or stability.

What’s at Risk for the Banking Industry

The ICBA and other world banking groups say that stablecoins that aren’t regulated could hurt financial stability, consumer protections, and anti-money-laundering controls.

They say that strong, well-thought-out oversight is needed to keep new risks from getting into the larger financial system.

Crypto companies say that a cautious, innovation-friendly approach to regulation is needed to make digital payments safer and easier for people who don’t have bank accounts to use.

Coinbase’s Push for a Banking-Like Path

Through a national trust charter, Coinbase has shown that it wants to work like a bank.

If this is approved, it would be a big change because it would let a company that focusses on cryptocurrencies work within the main parts of the U.S. financial system.

Critics, like the ICBA, say that this kind of move could make it harder to tell the difference between regular banks and crypto companies, and they want stricter rules.

Coinbase says that stablecoins and crypto payments can work with a strong, regulated system, not against it.

The GENIUS Act: A Way to Make Things Clear

Supporters of a clearer regulatory path point to laws like the GENIUS Act, which would put dollar-backed stablecoins under the control of the OCC and put strong protections in place.

Supporters say that this method would offer the protections that are needed while also showing innovators a clear way to move forward.

They say that a lot of banks are already looking into or using stablecoins, which means that a framework that looks ahead could help the market become less fragmented and confusing.

The Policy Debate and Paradigm

Paradigm, the company that helps Coinbase with its policies, fights back against what it calls “bad-faith” opposition from some traditional bank lobbies.

They say that the current resistance is like past tech pushbacks, when new technologies eventually found their place with the right safety measures.

From Paradigm’s point of view, the argument is that stablecoins can be used with good risk controls to help growth, trust, and more people being able to use financial services.

A Request for Fair Rules

The main point of the policy conflict is a simple question: how to encourage new ideas without making the system more vulnerable.

People who support cryptocurrencies say that there should be clear and fair rules for disclosures, reserve management, and consumer protection.

Voices from the banking industry say that without strong protections, rapid growth could outpace risk management, which would hurt both consumers and the economy as a whole.

The Regulatory Horizon and What It Means

The OCC’s decision about Coinbase’s charter is still a key moment for how quickly U.S. regulators will let crypto companies into the traditional banking system.

In addition, proposed laws like the GENIUS Act could change how the federal government keeps an eye on stablecoins.

The outcome will have an effect on more than just banks and crypto companies. It will also have an effect on the economy as a whole, slowing down the process of making digital assets a part of everyday finance.

Looking Ahead: Working Together or Staying Tense

As stablecoins and other tokenised assets grow, the relationship between crypto innovators and traditional banks is likely to change in one of two ways: either more cooperation with clear rules or more friction as stakeholders push for stricter rules.

Both paths will change the rules and regulations and affect how quickly and in what direction digital finance will change for years to come.

In short, the OCC’s decision and the path of stablecoin regulation will set the pace for how traditional banks and crypto companies work together. They will have to find a balance between the promise of technological progress and the protections that keep the financial system stable and trustworthy.